By Lyndsey Stram, Regional Economist; Lecia Parks Langston, Senior Economist

“You have power over your mind — not outside events. Realize this, and you will find strength.” Marcus Aurelius

In the wake of the COVID-19 pandemic, businesses lost revenues and workers lost jobs. But because of the time it takes to collect and collate data, economists have been left without much information to quantify the economic impacts at the local level.

But there is one ray of data illumination. Claims for unemployment benefits are promptly available and provide information about a large cross section of the economy. This post will outline what light unemployment claims data sheds on the state of southeast Utah’s economy.

While not all workers are protected by unemployment insurance laws, roughly 95% of jobs are covered. This makes claims data an exceptional source of information about the economy. Not included under unemployment insurance laws are most self-employed workers, about half of agricultural employment, unpaid family workers, railroad personnel (covered separately) and many nonprofit organizations (such as churches). Also, some out-of-work employees may not have worked a sufficient work history to qualify for unemployment insurance benefits, but may file anyway.

Fortunately, in this time of economic distress, the social safety nets of the unemployment insurance program, special national COVID-19 funding and social programs are working together to keep workers’ income and well-being stable.

Unemployment claimants and the unemployed; they aren’t the same

Also, keep in mind that, in addition to individuals drawing unemployment benefits, the unemployment rate includes those entering and re-entering the workforce and non-covered groups without current employment. This means the number of “unemployed” will be greater than the number of claimants. In “normal” times, only about 40% of the “unemployed” are claiming benefits.

The generally reported unemployment rate also has a work-search requirement. If you haven’t made any minimal attempts to find work, you aren’t counted as “unemployed.”

Watch this Space

While this analysis won’t be updated on a regular basis, new data will be added to the data visualization on a weekly basis allowing readers to check back for the latest information.

An Unprecedented Event

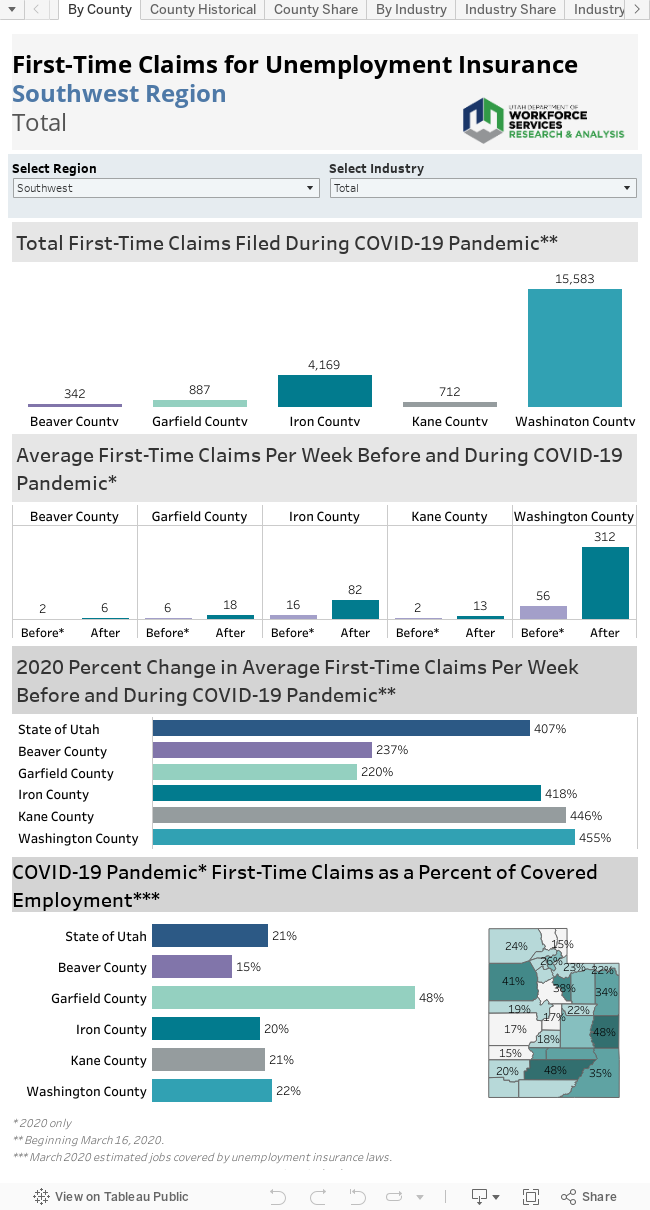

Not surprisingly, first-time claims for unemployment benefits soared in Utah and across the nation as the pandemic swept across the country. This increase is unprecedented since the creation of unemployment insurance coverage during the Great Depression. Week 12 (beginning March 16) marks the start of this unparalleled surge in claims. On a positive note, while new claims for unemployment insurance have skyrocketed in Utah, the state currently shows one of the lowest claims rates in the nation.

Most counties in the state saw the peak of first-time unemployment claims in weeks 13 and 14, 1-2 weeks after the COVID-19 pandemic hit, and this was true of San Juan County. Grand County however, with its large majority share of unemployment dependent on tourism related industries, saw a peak right away in week 12.

Another way to note the unprecedented flood of new claims is to look at weekly averages. Prior to the COVID-19 pandemic, southeast Utah averaged 23 claims per week. This has since increased to 227 average weekly first-time claims for unemployment.

Who took the hardest hit?

Counties with economies that largely depend on tourism are feeling the greatest economic and employment shocks in the state. This is true of Grand County, where 22% of the covered workforce has filed a claim for unemployment insurance in the weeks since the COVID-19 pandemic hit. San Juan also has some dependence on tourism but has only seen 11% of its workforce file, in line with the state average.

Tourism and COVID-19

Especially in the early stages of the restrictions, this is a story of tourism-dependent industries. More than 38% of COVID-19-related initial claims filed in southeast Utah represented workers previously employed accommodations and food services. In addition, the true effect of the pandemic on this industry is masked by a large number of claims classified as industry “unknown” in the early days of the claims flood. Undoubtedly, many of these claims would rightfully be classified in accommodations/food services if the appropriate information were available.

The High and the Low

Although accommodations/food services has generated the largest number of southeast Utah initial claims in the COVID-19 time period, in percentage terms, other industries have actually suffered more. For example, in the extremely small management of companies industry, roughly 70% of workers have filed for claims. The administrative support/waste management/remediation industries, which include temporary employment firms, shows a first-time claims rate of 52%.

Public administration however, has held onto higher portions of its workforce. Only 9% of the covered workforce in that sector have recently filed claims for unemployment. This is positive for southeast Utah where a large portion of the workforce is employed in this sector.

In many areas, healthcare/social assistance has made up for a large share of claims with the cessation of elective medical services. Southeast Utah has not seen this effect and much of that sector has remained employed.

County by County

Grand County

• Prior to the COVID-19 pandemic, Grand County saw a weekly average of 13 first-time claims for unemployment. In the weeks since, this has increased to 169 average weekly claims.

• Spring generally brings the start to the busy tourism season in Grand County, making the timing of the restrictions particularly impactful to the area. Nearly 500 claims (and probably well over if there was complete information for the unknown industry claims) were filed by workers previously in the accommodations/food services sector. Arts/entertainment/recreation also accounts for nearly 100 claims.

• Transportation and warehousing are also important to Grand County. About 25% of the workers from that sector have also filed claims for unemployment insurance in the wake of COVID-19.

• Before COVID-19 restrictions were enacted, Grand County made up for 57% of the region’s unemployment claims. This has since increased to 75%.

San Juan County

• Prior to the COVID-19 pandemic, San Juan County saw a weekly average of 10 first-time claims for unemployment. In the weeks since, this has increased to 58 average weekly claims.

• Although less dependent than its neighbor, Grand County, San Juan also depends on tourism spending during the summer months. Accommodations/food services accounts for the large majority of the first-time claims for unemployment in the county. As a percentage of the covered workforce in that sector, 23% of workers have filed.

• Public administration is an important sector in San Juan County and a sector that has not yet seen major shocks from the pandemic. Only 3% of this large industry has filed claims in recent weeks.

• Before COVID-19 restrictions were enacted, San Juan County made up for 57% of the region’s unemployment claims. This has since decreased to 25%.

But there is one ray of data illumination. Claims for unemployment benefits are promptly available and provide information about a large cross section of the economy. This post will outline what light unemployment claims data sheds on the state of southeast Utah’s economy.

While not all workers are protected by unemployment insurance laws, roughly 95% of jobs are covered. This makes claims data an exceptional source of information about the economy. Not included under unemployment insurance laws are most self-employed workers, about half of agricultural employment, unpaid family workers, railroad personnel (covered separately) and many nonprofit organizations (such as churches). Also, some out-of-work employees may not have worked a sufficient work history to qualify for unemployment insurance benefits, but may file anyway.

Fortunately, in this time of economic distress, the social safety nets of the unemployment insurance program, special national COVID-19 funding and social programs are working together to keep workers’ income and well-being stable.

Unemployment claimants and the unemployed; they aren’t the same

Also, keep in mind that, in addition to individuals drawing unemployment benefits, the unemployment rate includes those entering and re-entering the workforce and non-covered groups without current employment. This means the number of “unemployed” will be greater than the number of claimants. In “normal” times, only about 40% of the “unemployed” are claiming benefits.

The generally reported unemployment rate also has a work-search requirement. If you haven’t made any minimal attempts to find work, you aren’t counted as “unemployed.”

Watch this Space

While this analysis won’t be updated on a regular basis, new data will be added to the data visualization on a weekly basis allowing readers to check back for the latest information.

An Unprecedented Event

Not surprisingly, first-time claims for unemployment benefits soared in Utah and across the nation as the pandemic swept across the country. This increase is unprecedented since the creation of unemployment insurance coverage during the Great Depression. Week 12 (beginning March 16) marks the start of this unparalleled surge in claims. On a positive note, while new claims for unemployment insurance have skyrocketed in Utah, the state currently shows one of the lowest claims rates in the nation.

Most counties in the state saw the peak of first-time unemployment claims in weeks 13 and 14, 1-2 weeks after the COVID-19 pandemic hit, and this was true of San Juan County. Grand County however, with its large majority share of unemployment dependent on tourism related industries, saw a peak right away in week 12.

Another way to note the unprecedented flood of new claims is to look at weekly averages. Prior to the COVID-19 pandemic, southeast Utah averaged 23 claims per week. This has since increased to 227 average weekly first-time claims for unemployment.

Who took the hardest hit?

Counties with economies that largely depend on tourism are feeling the greatest economic and employment shocks in the state. This is true of Grand County, where 22% of the covered workforce has filed a claim for unemployment insurance in the weeks since the COVID-19 pandemic hit. San Juan also has some dependence on tourism but has only seen 11% of its workforce file, in line with the state average.

Tourism and COVID-19

Especially in the early stages of the restrictions, this is a story of tourism-dependent industries. More than 38% of COVID-19-related initial claims filed in southeast Utah represented workers previously employed accommodations and food services. In addition, the true effect of the pandemic on this industry is masked by a large number of claims classified as industry “unknown” in the early days of the claims flood. Undoubtedly, many of these claims would rightfully be classified in accommodations/food services if the appropriate information were available.

The High and the Low

Although accommodations/food services has generated the largest number of southeast Utah initial claims in the COVID-19 time period, in percentage terms, other industries have actually suffered more. For example, in the extremely small management of companies industry, roughly 70% of workers have filed for claims. The administrative support/waste management/remediation industries, which include temporary employment firms, shows a first-time claims rate of 52%.

Public administration however, has held onto higher portions of its workforce. Only 9% of the covered workforce in that sector have recently filed claims for unemployment. This is positive for southeast Utah where a large portion of the workforce is employed in this sector.

In many areas, healthcare/social assistance has made up for a large share of claims with the cessation of elective medical services. Southeast Utah has not seen this effect and much of that sector has remained employed.

County by County

Grand County

• Prior to the COVID-19 pandemic, Grand County saw a weekly average of 13 first-time claims for unemployment. In the weeks since, this has increased to 169 average weekly claims.

• Spring generally brings the start to the busy tourism season in Grand County, making the timing of the restrictions particularly impactful to the area. Nearly 500 claims (and probably well over if there was complete information for the unknown industry claims) were filed by workers previously in the accommodations/food services sector. Arts/entertainment/recreation also accounts for nearly 100 claims.

• Transportation and warehousing are also important to Grand County. About 25% of the workers from that sector have also filed claims for unemployment insurance in the wake of COVID-19.

• Before COVID-19 restrictions were enacted, Grand County made up for 57% of the region’s unemployment claims. This has since increased to 75%.

San Juan County

• Prior to the COVID-19 pandemic, San Juan County saw a weekly average of 10 first-time claims for unemployment. In the weeks since, this has increased to 58 average weekly claims.

• Although less dependent than its neighbor, Grand County, San Juan also depends on tourism spending during the summer months. Accommodations/food services accounts for the large majority of the first-time claims for unemployment in the county. As a percentage of the covered workforce in that sector, 23% of workers have filed.

• Public administration is an important sector in San Juan County and a sector that has not yet seen major shocks from the pandemic. Only 3% of this large industry has filed claims in recent weeks.

• Before COVID-19 restrictions were enacted, San Juan County made up for 57% of the region’s unemployment claims. This has since decreased to 25%.